PSC has evaluated the impact of the revised fiscal year 2013 sequestration targets mandated under the “fiscal cliff” legislation signed on January 2, 2013.

|

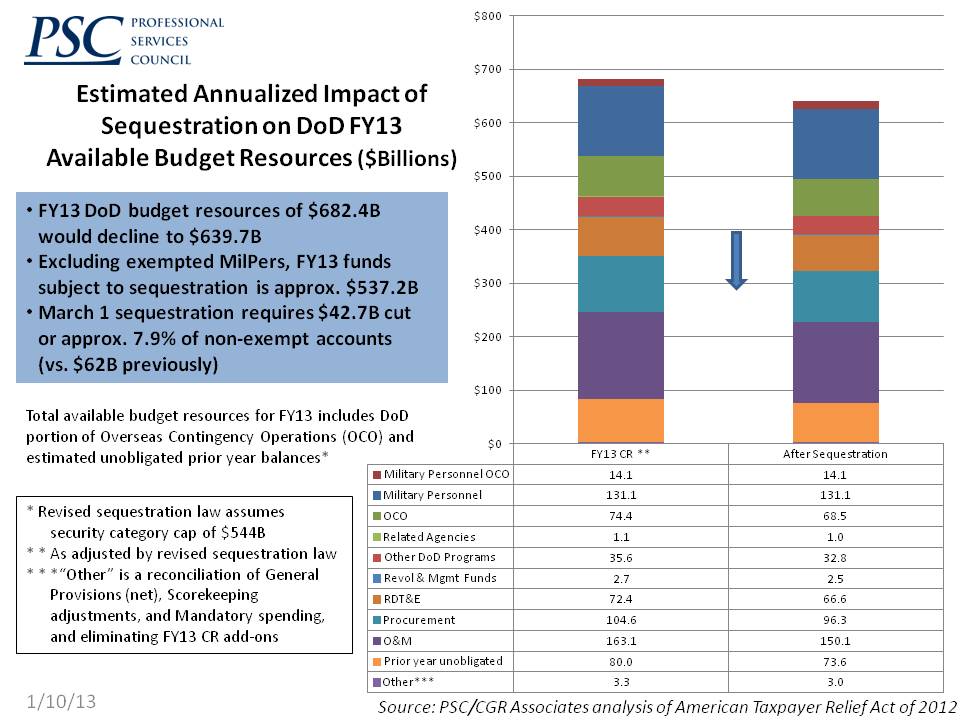

| Defense impacts. |

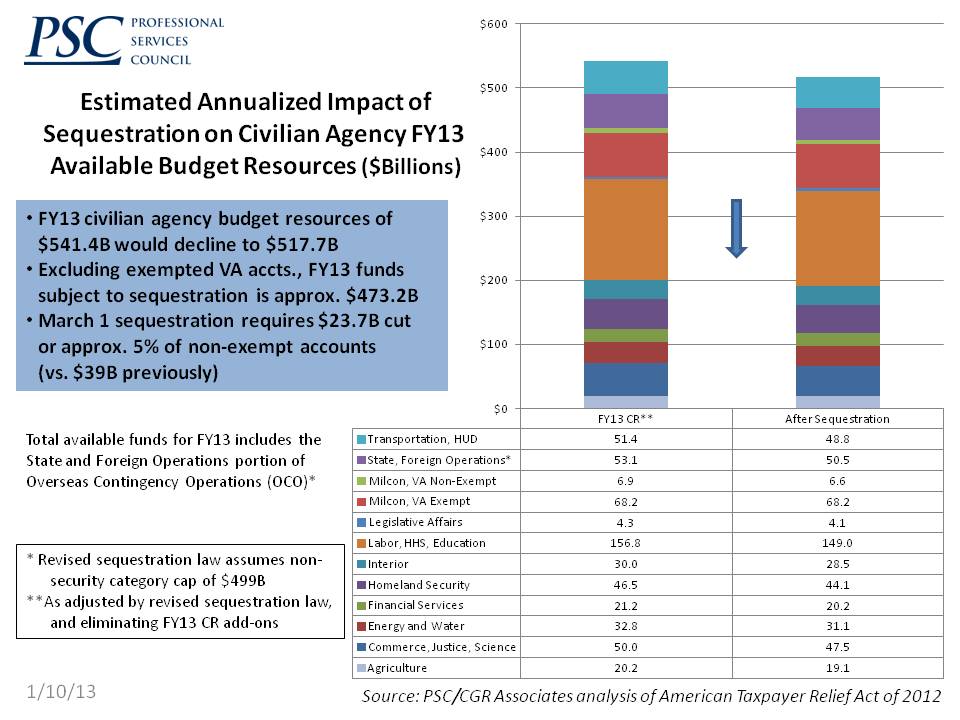

This law now requires the president to order a sequestration on March 1, 2013, with the potential for an additional sequestration action to be “evaluated and implemented” on March 27, 2013 if additional spending reductions are not achieved. Unless modified by a subsequent law, the discretionary spending savings required to be achieved through sequestration from March 1 through September 30, 2013 is $24 billion below the current level of discretionary spending reductions of $109.4 billion, providing a reduction to $85.4 billion, with approximately $42.7 billion coming from the “defense” category, $23.7 billion coming from the “non-defense discretionary” category, and $19 billion coming from certain non-defense mandatory spending programs.

|

| Civilian agency impacts. |

According to PSC’s analysis of these changes, every Department of Defense “program, project and activity” would have to be reduced by 7.9 percent on an annualized basis to achieve the required savings. Similarly, every non-defense “program, project and activity” would have to be reduced by 5 percent on an annualized basis to achieve the required savings.

This law also extends into fiscal year 2014 the “firewall” between security and non-security discretionary spending that was due to phase out after fiscal year 2013. It also further reduces the overall discretionary spending in fiscal year 2014 by $8 billion, from $1.066 trillion to $1.058 trillion, with security discretionary spending capped at $552 billion and non-security discretionary spending capped at $506 billion.

PSC's previous calculations are available

here and

here for comparison.

A version of this story first appeared in the new PSC newsletter, PSC Now. Read this and other PSC news here.